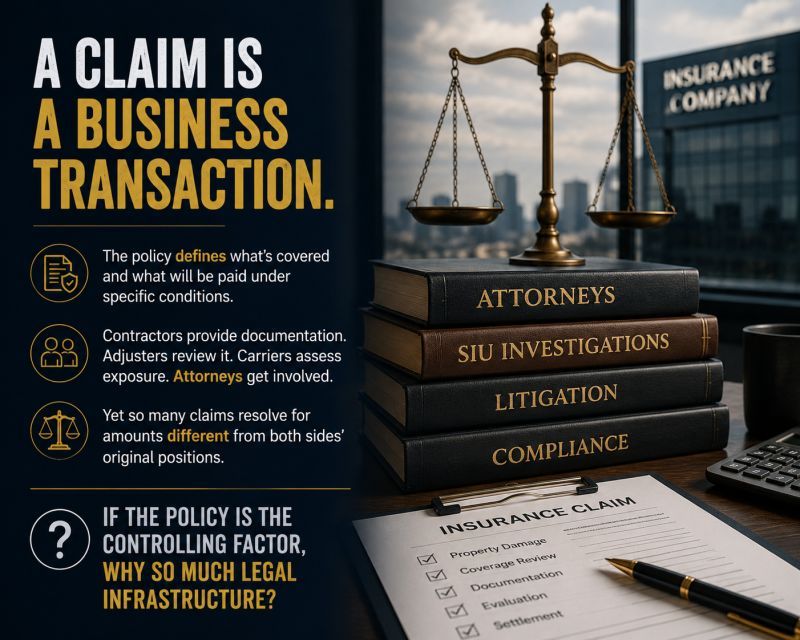

A Claim is a Business Transaction

One thing I've noticed when looking at insurance company personnel on LinkedIn is just how many people work in legal or investigative roles.

SIU investigators. Attorneys. Paralegals. Litigation specialists. Compliance personnel. Coverage counsel.

In many cases, it seems like a significant portion of the visible workforce is dedicated to managing legal exposure and liability.

That raises a question.

If an insurance policy is a contract that clearly outlines what is covered and what should be paid when certain conditions are met, why is such a large legal infrastructure necessary?

Over the years, I've become convinced that an insurance claim is ultimately a business transaction. Contractors present documentation. Adjusters review it. Carriers evaluate exposure. Attorneys become involved when disagreements arise.

What I've found interesting is that claims frequently settle for amounts that differ from the original positions taken by either side. Sometimes more. Sometimes less. Often after substantial time, expense, and effort.

If the policy language is the controlling factor, why do so many claims require extensive legal involvement before reaching a resolution?

I'm genuinely curious how others in the industry view this.

Is the large legal presence primarily about ensuring compliance with the policy contract, or is it more about managing corporate liability and financial risk?

Where do you think the balance should be?

- Jason Husk, CEO of Managed Chaos Restoration Services (MCRS)